我们不再支持这个浏览器. 使用受支持的浏览器将提供更好的体验.

请 更新浏览器.

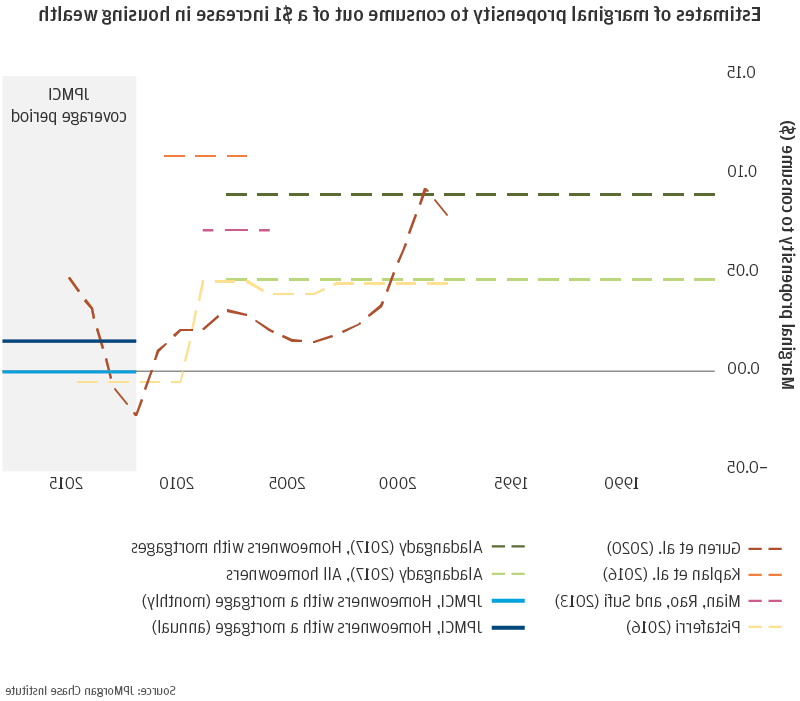

在美国,大约三分之二的家庭都是这样.S. 拥有一个家. 不断上涨的房价,以及由此带来的住房财富,可以刺激家庭消费. 因此,房地产市场可以对更广泛的经济产生重大影响. 从20世纪90年代末到经济大衰退, estimates of the marginal propensity to consume (MPC) out of housing wealth range from approximately 4 cents to 9 cents, 大衰退时期的研究发现mpc高达11美分.1 然而, evidence of slower-than-expected consumption and GDP growth in combination with relatively low levels of home equity extraction after the Great Recession suggest that the housing wealth effect may be much smaller after the financial crisis than for prior periods. 事实上, 最近的一些研究表明,货币政策委员会的利率可能低至零, 但是这些研究并没有提供精确的因果估计.

在这份报告中, we answer the following research question: What was the household consumption response to the 50 percent increase in housing wealth in the post-Great Recession period? 我们链接去识别的银行数据, 包括交易级存款账户和信用卡数据, 到贷款级抵押贷款数据,以估计2012年至2018年期间MPC的住房财富. Our large sample and direct measure of consumption allow us to derive more precise MPC estimates than otherwise available.

The marginal propensity to consume is the proportion of an increase in income or wealth that a consumer chooses to spend on goods and services rather than save.

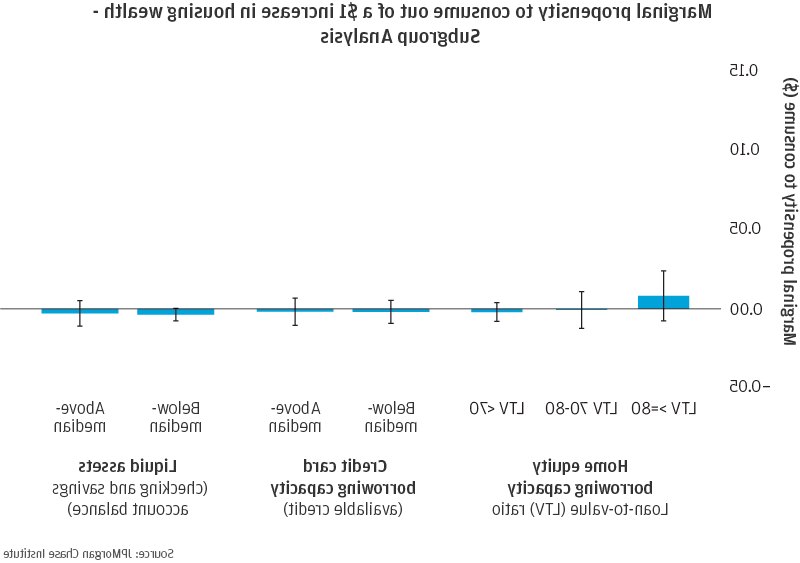

来自2012年至2018年期间超过1600万大通抵押贷款客户的数据, 样本值为1.7 million customers who had both a 追逐 mortgage and 追逐 deposit account during that period and who fulfilled other criteria described above. 我们的贷款级抵押贷款数据使我们能够观察到每个房主的贷款细节.g.(当前权益水平). 在稳健性检查中, we also examined a sample of over 5 million 追逐 credit card customers who are likely to be homeowners according to information on their credit card application. 类似的研究估计了住房财富对之前时期mpc的影响, we use an instrumental variables strategy with housing supply elasticity as the instrument to derive causal estimates.

影响

How do we reconcile the much smaller MPC out of housing wealth in the post-Great Recession period with a larger MPC during the preceding periods? We find that the volume of equity withdrawal in the post-Great Recession period was much lower than during the housing boom. 研究表明,需求和供给因素都在起作用. 金融危机之后, a larger share of equity became concentrated in the hands of older and less credit-constrained borrowers who tend to have a lower demand for equity extraction. 同时, tightened lending standards have reduced the supply of credit to more credit-constrained mortgage holders who may have greater demand for equity extraction. We contribute new evidence that a lack of demand to borrow against home equity contributed to a low marginal propensity to consume out of housing wealth: even homeowners with more equity (for whom it should be easy to borrow) did not consume more when housing wealth rose.

This research has several implications for policymakers and is particularly relevant as the economy comes to face a severe recession induced by the 新型冠状病毒肺炎 pandemic. 第一个, homeowners entered the 新型冠状病毒肺炎 crisis with a substantial amount of illiquid wealth in the form of home equity. Given the importance of cash flow dynamics and liquidity as determinants of consumption and the ability to stay current on housing payments, 允许房主在面临财务困境时保留或增加流动性的措施, 比如通过忍耐或维持获得房屋净值, 能否提供重要的财政缓冲. 这些类型的措施带有风险, 然而, 因为房价可能会在经济衰退中贬值, eroding the equity position of homeowners—and increased income volatility could make it more difficult for borrowers to meet debt obligations.

第二个, a much smaller housing wealth effect diminishes the ability of conventional monetary policy—changes to short-term interest rates—to affect the real economy through the housing market, 导致消费和GDP增长低于政策制定者可能预期或希望刺激的水平. 住房财富效应MPC是否保持在衰退前的估计水平, 我们发现消费和GDP等于0.1 to 1.5%和0.从2012年到2018年,每年分别增长1%到1%.2 像这样, policymakers may need to lean more heavily on other channels of monetary policy and unconventional measures, 以及在经济低迷时期为家庭提供流动性的财政政策.